An inverted Treasury yield curve has historically been one of Wall Street’s more reliable recession indicators. But it has been flashing for more than a year now, with little sign of an economic slowdown in sight.

However, that could soon change, according to one Wall Street economist.

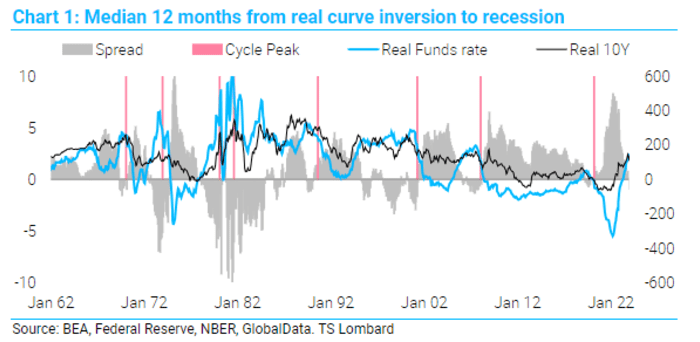

While the nominal yield curve has been inverted since 2022, the real yield curve only inverted for the first time since the Fed kicked off its latest rate-hiking cycle last month, according to Steve Blitz, chief U.S. economist at TSLombard.

Real yields are adjusted for inflation. The Treasury yield curve is a line drawn across the yields of all Treasury maturities. Typically, yield curves slope upward, with investors demanding more compensation for lending money over a longer period. An inverted curve happens when the yield on shorter-dated maturities rise above yields on longer-dated maturities.

Assuming a recession does eventually materialize, this could help explain why an indicator that has preceded every recession since the 1960s — including, as it would happen, the surprise COVID-19-induced recession in 2020 — appeared to misfire.

Previously, the nominal and real yield curves inverted almost simultaneously. But this time, more than a year passed between them, Blitz said.

“What happened to the yield curve as predictor? Simply put, in prior cycles the nominal and real yield curves generally moved in sync, so there was no need to differentiate,” Blitz said in a note to clients shared with MarketWatch on Thursday.

“This time, the nominal curve flipped a year ago, but the real curve only just inverted in January. The real curve matters more because recessions occur more predictably after they invert,” he wrote.

TSLOMBARD

Blitz’s report comes at a time when real interest rates have been a key issue for market-watchers and economists. Late last month, a report in The Wall Street Journal warned that the Fed faced a new dilemma by keeping interest rates elevated with inflation on the wane.

The risk, according to the report, is that swiftly easing inflation could cause real short-term rates to rise, potentially heaping more pressure on the economy if the Fed doesn’t lower interest rates accordingly.

Inflation has waned rapidly since it reached its fastest rate in four decades during the summer of 2022. According to the December PCE Price Index, the Federal Reserve’s preferred inflation gauge, shows the rate of core inflation has slowed to 1.9% annualized over the past six months.

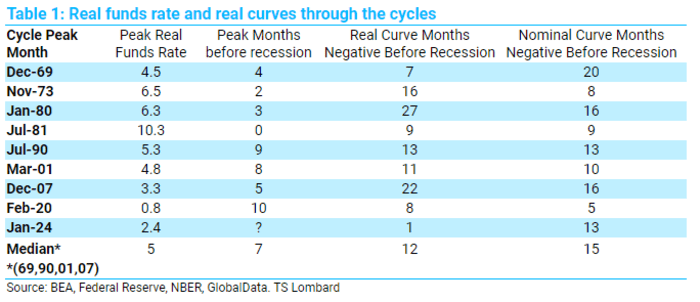

According to Blitz’s data, the median length of time it has taken for a U.S. recession to begin following the inversion of real interest rates is 12 months, compared with 15 months for the nominal yield curve. If this holds, then a recession should begin late in 2024 or early 2025.

TSLOMBARD

Dow Jones Market Data shows the three-month T-bill yield, which is roughly equivalent to the effective fed-funds rate, has been higher than the yield on the 10-year Treasury note since Nov. 8, 2022 — about 15 months.

That is the longest stretch of uninterrupted inversion going back to 1989, the earliest data available. But the spread between the two-year yield and 10-year yield has been inverted for even longer, since July 2022.

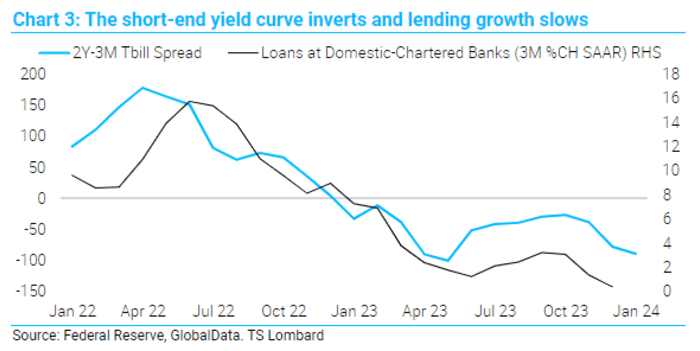

An inverted yield curve has caused loan growth in the U.S. economy to slow practically to zero, Blitz said. But now that the real yield curve has inverted, the rate of change in lending by U.S. banks could soon turn negative. Banks shrinking their loan books, as opposed to holding them constant or growing them, would deal a blow to the real economy.

TSLOMBARD

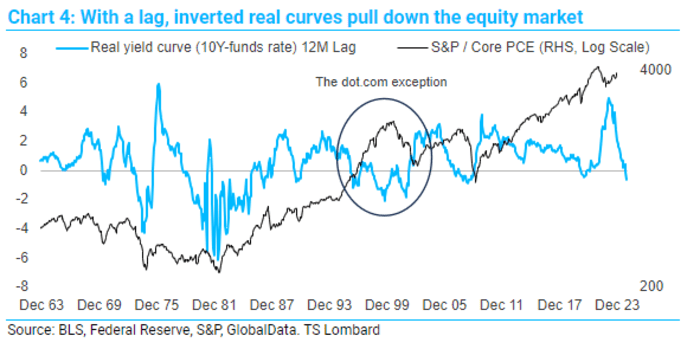

The inverted real yield curve could also hurt the stock market, Blitz pointed out, again citing historical data.

“Inverted real curves have a lagged behind negative impact on the equity market — not surprisingly about 12 months later, the same median length from real inversion to recession,” he said.

TSLOMBARD

To find an example that mirrors the circumstances that the Fed now finds itself in, Blitz had to look all the way back to the late 1960s and the policy decisions that led to a recession in late 1969. Back then, the real curve only turned negative after the nominal curve had been inverted for 13 months.

The fact that this episode was followed by the great inflation of the 1970s suggests that the Fed is justified in wanting more evidence that inflation is trending back toward its 2% target, Blitz said.

The nominal yield curve was un-inverting a touch on Thursday, with the three-month T-bill yield

BX:TMUBMUSD03M

moving marginally lower, while the yield on the 10-year Treasury note

BX:TMUBMUSD10Y

rose by 4 basis points to 4.16%.

U.S. stocks looked set to finish higher on Thursday, with the S&P 500

SPX

up 0.1% at 4,997, leaving the index on the cusp of surpassing 5,000 for the first time ever. Meanwhile, the Dow Jones Industrial Average

DJIA

gained 30 points, or 0.1%, to 38709. The Nasdaq Composite

COMP

rose by 0.3% at 15,800.